linmix Math¶

Linmix is a hierarchical Bayesian model for fitting a straight line to data with errors in both the x and y directions. This model is described in detail by Kelly (2007) available here: http://arxiv.org/abs/0705.2774. The paper describes both univariate and multivariate models; since we have only implemented the univariate model to date, we only describe that model here.

The observed independent (\(x\)) and dependent (\(y\)) variables are assumed to be drawn from a 2-dimensional Gaussian distribution:

with mean \(\mu = (\xi, \eta)\), which describe the unobserved true values the independent and dependent variables, and covariance matrix \(\Sigma = \left(\begin{smallmatrix} \sigma_x^2& \sigma_{xy} \\ \sigma_{xy} & \sigma_y^2 \end{smallmatrix}\right)\), where \(\sigma_x\) and \(\sigma_y\) are the \(x\) and \(y\) 1-sigma Gaussian errors and \(\sigma_{xy}\) is the covariance between \(x\) and \(y\).

The unobserved true independent and dependent variables are related by

where \(\alpha\) and \(\beta\) are the intercept and slope of the regression line and \(\sigma^2\) is the Gaussian intrinsic scatter of \(\eta\) around the regression line. The priors on the regression parameters \(\alpha\), \(\beta\), and \(\sigma^2\) are given as uniform.

The model for the distribution of the latent independent variable is a Gaussian mixture, which is both flexible and computationally manageable. The mixture is defined by the component probabilities \(\pi\), component means \(\mu\) and component variances \(\tau^2\):

The distribution of the mixture parameters \(\pi\), \(\mu\) and \(\tau^2\) are described by additional layers of the hierarchy:

Note that we additionally truncate the domain of \(u^2\) to be \([0, 1.5 \mathrm{Var}(x)]\), as described in the notes of Brandon Kelly’s IDL program LINMIX_ERR.pro.

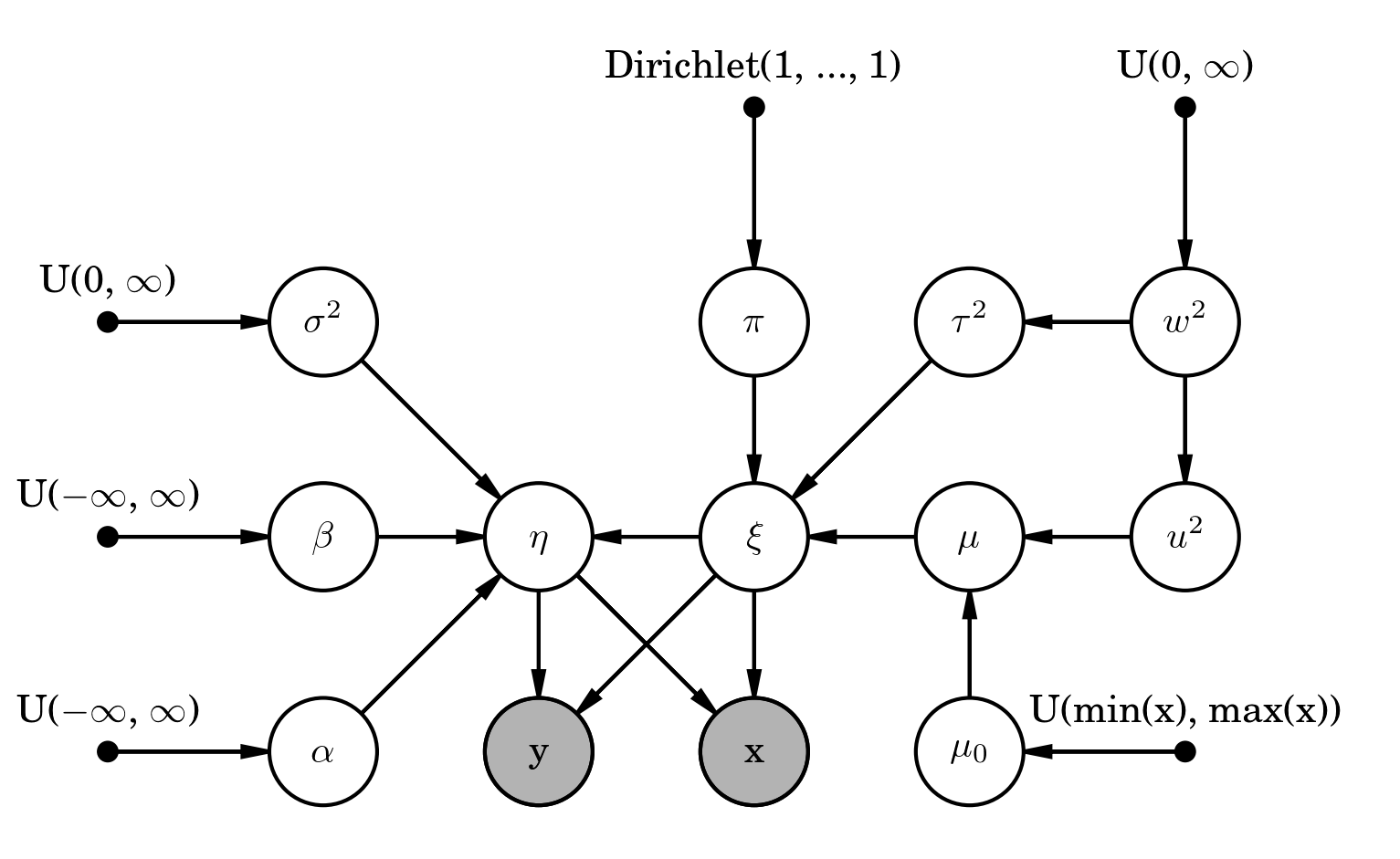

The entire model can be summarized by the following probabilistic graphical model: